The team behind the privacy-obsessed bitcoin app, Samourai Wallet, has gotten its first round of venture funding.

Founded by two former developers at Blockchain.info, Keonne Rodriguez and William Hill, the wallet’s maintainer, Katana Cryptographic, has received a $100,000 investment from Cypherpunk Holdings.

Samourai Wallet has been built for Android users, specifically designed to enhance privacy while using bitcoin.

“There is no other cryptocurrency that is as battle-tested and hardened as bitcoin,” Rodriguez, Katana’s director, told CoinDesk in an email. “The founding team of Samourai has zero interest in working on other coins, or even other layers of bitcoin at this time.”

The wallet has a number of features that provide greater privacy for users, such as a service that puts intermediary hops in a transaction in order to create uncertainty about which wallet pays for what. Another feature makes it difficult to trace the provenance of someone’s bitcoin. The company earns a small fee, in bitcoin, from users that make use of these services.

Samourai also provides a privacy-enhancing service called “stonewall” for free. Stonewall creates doubt about the ownership of bitcoin in a given transaction. The company is also offering a forthcoming hardware product, called Dojo, which is a user-friendly bitcoin node built to work with the wallet. High marks

Still an alpha release in the works since 2015, Samourai has 27,000 users, according to the company. Its first full version should come out in June. Rodriguez said it will use the funding to expand its development, customer service and quality assurance program, all of which have been put under significant pressure by the wallet’s growth.

The products have personally impressed John Carvalho, a longtime bitcoin user who currently works at Bitrefill. Carvalho told CoinDesk:

“I have respect for any company that adds utility for Bitcoiners and Samourai is clearly willing to go against the grain to add privacy options for users. If Bitcoin is freedom money, Samourai are freedom fighters.”

A similar sentiment spurred the investment itself. Cypherpunk, a venture fund listed on the Canadian Securities Exchange under the ticker symbol HODL, was set up as an investment vehicle to support privacy-enhancing technology.

Deal Emphasizes Cypherpunk's Commitment to Funding Outstanding Privacy Technology

Toronto, Ontario--(Newsfile Corp. - June 3, 2019) - Cypherpunk Holdings Inc. (CSE: HODL) ("Cypherpunk" or the "Company") is pleased to announce it has become the lead investor in Katana Cryptographic Ltd., whose main product is Samourai Wallet

Katana Cryptographic is an early-stage, London-based computer software company, focused on developing privacy technologies. Katana has developed numerous algorithms and actively maintains open source software designed to mitigate against common surveillance tactics and enhance transactional privacy.

Its main product, Samourai Wallet, is described by the coinsutra.com as "the most secure and privacy-centric Bitcoin wallet currently available in the market." Samourai is still in alpha-mode, but it already has a user-base of 27,000. Full-release 1.0 is expected before the end of June.

Katana's founders, Keonne Rodriguez and William Hill, were, respectively, Product Lead and Lead Mobile Developer at blockchain.info between 2013 and 2016, overseeing the growth of the user-base from from 1m to 6m.

Other Katana privacy technologies include Open Exploration Tool, Ricochet, Stonewall,Whirlpool and Dojo.

Commentating on the investment, Cypherpunk Director Dominic Frisby said: "We met with Katana, and were most impressed with the technologies they are developing and with Katana's commitment to privacy. We share similar values, so are delighted to be able to aid the future development of Katana's products from such an early stage. This deal shows the edge that we at Cypherpunk have."

Cypherpunk Chief Economist Jon Matonis added: "As transactional privacy by default becomes the norm in digital wallets, Samourai may be leading the way in fungibility innovation and maintaining proper coin hygiene."

Katana's CEO Keonne Rodriguez commented, "Katana is excited to have found a partner in Cypherpunk Holdings. We look forward to their partnership and support as we continue executing on our mission to deploy easy to use, privacy enhancing software on the Bitcoin blockchain. Financial sovereignty is more important now than ever before, with the freedom to transact being tantamount to freedom of speech. Cypherpunk Holdings have demonstrated their commitment to these core values and we look forward to working on delivering this vision with their support."

Cypherpunk Holdings Inc. is a vehicle set up to invest in companies, technologies and protocols, which enhance or protect privacy. Its strategy is to make targeted investments in businesses and assets with strong privacy, often within the blockchain ecosystem, including select cryptocurrencies. The stated mission of Cypherpunk Holdings is "to become the world's leading privacy-focused investment vehicle." This is a seed capital investment of US $100,000.

Cypherpunk's common shares trade on the Canadian Securities Exchange under the symbol "HODL".

Cautionary Note Regarding Forward-Looking Information

This news release contains "forward-looking information" within the meaning of applicable securities laws. Generally, any statements that are not historical facts may contain forward-looking information, and forward-looking information can be identified by the use of forward-looking terminology such as "plans", "expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates" or "does not anticipate", or "believes", or variations of such words and phrases or indicates that certain actions, events or results "may", "could", "would", "might" or "will be" taken, "occur" or "be achieved". Forward-looking information includes, but is not limited to the Company's goal of making investments in the blockchain and other sectors and enhancing value. There is no assurance that the Company's plans or objectives will be implemented as set out herein, or at all. Forward-looking information is based on certain factors and assumptions the Company believes to be reasonable at the time such statements are made and is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking information. There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information. Forward-looking statements are made based on management's beliefs, estimates and opinions on the date that statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, except as required by law. Investors are cautioned against attributing undue certainty to forward-looking statements.

Investor Relations Contact: Marc Henderson, Interim President and Chief Executive Officer, Cypherpunk Holdings Inc., Office: 416.599.8547

Toronto, Ontario--(Newsfile Corp. - February 13, 2019) - Cypherpunk Holdings Inc (CSE: HODL) ("Cypherpunk" or the "Company") is pleased to announce that Jon Matonis has joined the company as Chief Economist. Jon Matonis is a monetary economist with a particular focus on non-political digital currencies and privacy technologies. His career has included senior influential posts at VISA International, VeriSign, Sumitomo Bank and Hushmail. He was a founding director of the Bitcoin Foundation.

Commenting on his appointment, Matonis said, "The financing and support of privacy technologies is more important now than ever before in history. I am honored to join the team effort at Cypherpunk Holdings in funding those critical projects that not only should prevail, but that must prevail."

Cypherpunk interim CEO, Marc Henderson, said, "Jon Matonis is one of the foremost intellects in the blockchain, cryptocurrency and privacy technology sector. This appointment at such an early stage in the evolution of Cypherpunk Holdings shows the scope of what we are looking to achieve with this company. We are delighted that Jon is onboard with that. Things are starting to move forward, and we are very excited. We are hoping to make further announcements in the coming weeks."

Cypherpunk Holdings Inc is a Canadian-based holding vehicle set up to invest in companies, technologies and protocols, which enhance or protect privacy, as well as freedom and trust. Its strategy is to make targeted investments in and acquisitions of businesses and assets with strong privacy, often within the blockchain ecosystem, including select cryptocurrencies. The company believes privacy will be an increasingly strong narrative across the technology sector going forward.

The stated mission of Cypherpunk Holdings is "to become the world's leading privacy-focused investment vehicle." More details, and the latest company presentation, can be found at the company website: https://cypherpunkholdings.com/.

Jon Matonis is an economist and e-Money researcher. He serves as an independent board director to companies in the Bitcoin, the Blockchain, mobile payments, and gaming sectors. He has been a featured guest on CNN, CNBC, Bloomberg, NPR, Al Jazeera, RT, Virgin Radio, and numerous podcasts. As a prominent fintech columnist with Forbes Magazine, American Banker, and CoinDesk, he recently joined the editorial board for the cryptocurrency journal, Ledger. His early work on digital cash systems and financial cryptography has been published by Dow Jones and the London School of Economics.

Matonis advocates worldwide for Bitcoin to a wide variety of audiences, including members of the Federal Reserve Bank, the Bank of England, the European Central Bank, SWIFT, the US Department of Justice, retail payment networks, major financial institutions, financial regulatory bodies, mobile money issuers, iGaming operators, information security firms, hedge funds, gold investors, and family offices.

The Company has today granted a total of 900,000 options to purchase shares of the company at a price of $0.07 per share until June 1, 2023.

Following its recent name change to Cypherpunk Holdings, the Company's common shares trade on the Canadian Securities Exchange under the symbol "HODL". The new name references the important contribution of the Cypherpunks and the Cypherpunk Manifesto to the development and ultimate emergence of cryptocurrencies.

Cautionary Note Regarding Forward-Looking Information

This news release contains "forward-looking information" within the meaning of applicable securities laws. Generally, any statements that are not historical facts may contain forward-looking information, and forward-looking information can be identified by the use of forward-looking terminology such as "plans", "expects" or "does not expect", "is expected", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates" or "does not anticipate", or "believes", or variations of such words and phrases or indicates that certain actions, events or results "may", "could", "would", "might" or "will be" taken, "occur" or "be achieved". Forward-looking information includes, but is not limited to the Company's goal of making investments in the blockchain and other sectors and enhancing value. There is no assurance that the Company's plans or objectives will be implemented as set out herein, or at all. Forward-looking information is based on certain factors and assumptions the Company believes to be reasonable at the time such statements are made and is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking information. There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information. Forward-looking statements are made based on management's beliefs, estimates and opinions on the date that statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, except as required by law. Investors are cautioned against attributing undue certainty to forward-looking statements.

Investor Relations Contacts:

Marc Henderson

Cypherpunk Holdings Inc.

Interim President and Chief Executive Officer

Office: 416.599.8547

From: Satoshi Nakamoto Subject: Re: Introduction To: “Jon Matonis” Date: Thursday, March 4, 2010, 9:55 PM

Nice blog. That’s the first I’ve seen that focuses on this subject. I wish there was something like that when I originally researched this three years ago, there was scant to nothing back then. I think I’ll be a regular reader.

Bitcoin would be right up your alley. Its advantage is that it’s P2P. There isn’t a central mint or company running it. As long as there are users, it survives.

I’m sure you’ve already found the FAQ and Forum at bitcoin.org.

The logo is here:

http://www.bitcoin.o….php?topic=64.0

Was there anything particular you were interested in?

What about off-shore tax havens? Tax lawyers, accountants, and financial and tax consultants sooner or later hear this question. Why the query? Those asking about foreign tax havens are interested in:

secrecy in existence of property,

secrecy in existence of income,

security of property from predators such as governments and legitimate creditors, or

the few remaining esoteric, legitimate tax savings available through international tax planning.

The questioner never cares about the fourth reason. The other three per se do not involve criminal behavior but would if the existence of the tax haven cache or scheme were denied on a tax form or at a conference, examination, or hearing. There is nothing illegal, even under our oppressive law, about a foreign bank account. The law is violated when a citizen confesses on a government form and lies about the off-shore bank account or entity—for example, when the haven seeker files a financial statement as the result of judicial proceedings enforcing an Internal Revenue Service summons and the financial statement understates assets by the amount on deposit in George Town, Cayman Islands.

But who will know—right? Wrong!

Who will know could easily be the Intelligence Division of the IRS. A few years ago, IRS special agents implemented "Project Leprechaun" in Nassau, George Town, and Miami. They had passwords and countersigns. Their lock picks and vans with electronic impedimenta were so sophisticated that the Impossible Mission Force would have been green with envy. The IRS hired prostitutes and gave them the code name "The Mata Hari Corps." Mata would entertain a bank official while Harry would pilfer the john's briefcase for the book with secret account numbers and, in some cases, code names that go with those numbers. In some cases, the IRS agent would look for the names of shareholders in secret haven corporations. Prostitutes were paid out of the Treasury of the United States—literally for once, and not just figuratively. The IRS is continuing its investigation of foreign tax havens with the same lack of gentlemanly courtesy.

IN SEARCH OF SECRECY

Three of these reasons for interest in foreign tax havens center on that precious and elusive quality: anonymity. Yet anonymity, both in the existence of property and in the existence of income, is not as certain as promoters of foreign tax havens have proclaimed. The culprits are the French, notoriously the most adept tax cheaters on the planet.

The French have sought the sanctuary of neighboring Switzerland to hide their wealth from the French Recezeur des Contributions Directes, whose appetite is just as insatiable as that of the Internal Revenue Service. The Swiss yielded to pressure from the governments of France and other nations. Within the last five years Switzerland and the Cayman Islands, a British Crown Colony—the two most popular tax havens for Americans—have set up the machinery to disclose information to nosy government agents. In Switzerland, this machinery takes the form of mutual disclosure treaties. In the Caymans, which have no such treaty with the United States, it takes the form of a new Caymanian law.

Under the new law, any government authority can gain access to Caymanian bank records upon the filing of an affidavit alleging behavior that would be a crime in the Cayman Islands. Although tax evasion is not a crime by Caymanian lights, there are enough crimes common to both the United States and the Gulf tax haven to enable the IRS or the FBI to swear to an entire buffet of criminal behavior instead of tax evasion, and government agents have been known to lie under oath when they really want to "get" somebody.

For access to Swiss banking records, all the IRS need do is claim that the depositor is suspected of tax fraud. The linguistic Swiss, however, through a decision of their federal supreme court, distinguish between tax fraud and simple tax evasion. The former is discoverable under the treaty; the latter is not. Most of what the IRS calls tax fraud, the Swiss call simple tax evasion, and privacy survives in spite of a treaty with the United States. The point is, however: the legal machinery exists to enable the Swiss to divulge bank secrets to the US government. The assurances that this does not or likely will not happen are assurances of government officers who can vacillate—and perhaps even lie as well and as frequently as American government agents.

Yet many are still captivated by the mystique of foreign tax havens with tropical cohorts helping Americans keep wealth from official predators and Zurich bankers regaling visitors with tales of international intrigue involving state treasuries purloined by escaping dictators. Then too, there is the status achieved when one has a foreign bank account or off-shore corporation.

While the prevailing motivation for fascination in foreign tax machinations is anonymity, the need for it becomes critical precisely when a government investigator, lawyer, or judge asks the direct question, "Do you own or have an interest in a foreign bank account or entity?"—a question that can evoke only three answers: "Yes"; "I refuse to answer on the grounds that my answer may tend to incriminate me"; and "No."

The "No" answer would be a lie under oath and the crime of perjury. True, there is virtually no chance of "getting caught" with sophisticated foreign tax planning; however, the anonymity becomes vital to prevent prosecution, and foreign government agents are still government agents and therefore cannot be trusted.

If that is not enough: property with a foreign locus is not portable. Portability is as important to those interested in foreign tax havens as is anonymity, and a foreign tax haven's main deficiency is that it is foreign.

WHY DIAMONDS?

The perfect tax haven is anonymous, portable, not foreign, liquid, and appreciating in value. It, of necessity, would be property of intrinsic value. Gold and silver have too much mass in relation to value to be portable. Art treasures are not liquid. The ideal tax haven is one that is the property itself, property that combines anonymity, portability, availability, and liquidity. And what property haven meets these criteria? Diamonds.

Over the last seven years, diamonds of investment quality have appreciated in value, on the average, better than 25 percent per year. The prospect for more appreciation is even greater.

Inflation increases the value of diamonds, as does whatever happens in Africa. South Africans are buying and hiding diamonds, thereby reducing the supply. Miners must dig deeper into the volcanic pipe to find diamonds. Diamonds found deep in the pipe are poorer in clarity and color than those found near the surface. (The 44.5 carat Hope Diamond was found in a stream in India!) Black majority rule in South Africa, especially if won by rebellion or invasion, most likely would trigger the flooding of the diamond mines with water kept out only by the skill and technology of white Afrikaaner technicians. This is precisely what happened in Angola a few years ago.

The market, uninfluenced by any government and therefore free, in one sense, is yet manipulated upward by the supplier, DeBeers Consolidated Mines of South Africa. Liquidity, however, can still be a problem for short-term investment of less than 18 months, but as investor demand for diamonds continues to increase, so does liquidity.

The biggest obstacle to diamond investment is the mystery that surrounds diamonds and the resultant inability to be certain that the price of the diamonds purchased is the lowest possible price. This mystery can breed sharp practices and fraud.

Yet diamonds remain the hardest of the "hard money" and offer the investor more advantages than foreign tax havens. Hard-money advocates increasingly are adding investment-quality diamonds to their doomsday portfolios. The sparkle has been dulled, however, by certain cloudy practices that have crept into this, one of the fastest-growing new investment markets. Many investors are disappointed because, even though the price of investment diamonds has risen substantially, the resale value of their investment has not risen as much. In some cases, these investors find out a year later that it is difficult to sell the diamonds for what they paid for them and that they must wait 18 months or two years to realize a gain. Diamonds can be a good investment and a near-perfect hedge against inflation, but only if investors understand basic principles of diamond economics and if investment diamond houses avoid the temptation to exploit confusion. For the savvy investor dealing with the credible investment house, diamonds can be the best investment for these sorry times of government money grabbing, double-digit inflation, and monetary uncertainty.

DIAMOND SAVVY

Education in the investment diamond market starts with a basic understanding of these traps for the unwary:

Diamond dealers who don't know much more than neophytes about diamonds. The diamond market is virtually unregulated. There are no tests or requirements for becoming a diamond seller. And many people in this trade lack basic knowledge about the technology and economics of diamonds.

Antique shops, jewelry stores, gold and silver dealers, and pawnbrokers are becoming overnight "experts" in investment-grade diamonds. Usually having built up trust with the prospect from prior transactions, many of these part-time diamond dealers take advantage of that trust by overpricing. The diamond investor can protect against such overpricing by dealing only with professional diamond brokers selling only quality investment diamonds certified by the Gemological Institute of America (GIA), a nonprofit gem-grading laboratory located in New York City and in California in Los Angeles and Santa Monica.

The highest-quality diamonds, and generally the best investments, are called investment-grade, not to be confused with diamonds for jewelry, called cosmetic-grade, or with industrial diamonds. The primary keys to determining diamond quality are the four Cs: carat, color, clarity, and cut.

Carat is named after the tiny carob seed used since ancient times as a minuscule unit of measurement. A diamond's per carat value increases geometrically as the carat weight increases. So, a two-carat diamond of a particular clarity, color, and cut is worth more than two times the value of a one-carat diamond of the same clarity, color, and cut. Until recently, diamonds of less than one carat were not popular as investments in the United States, but that situation has changed, making the investment diamond market more accessible to small investors. An investor can purchase an investment-grade half-carat diamond for as low as $1,500. Currently, it takes $4,500 to start an investment portfolio with diamonds of one carat or larger.

Jewelers classify diamonds by color as white or blue-white, faint yellow, or other colors. True diamond professionals, however, do not grade colors with descriptive terms. In the language of the professional, the best diamond is not classified as white or blue-white. The highest color grade is D on the GIA color table for diamonds. A diamond is downgraded E, F, G, etc., as it takes on a color or becomes cloudy, losing what is called "the ice effect." To the untrained eye, these colors look alike. The only way a buyer can be sure of a diamond's color grade without actually matching it to comparison standard stones is to read the color rating on the GIA certificate. The optimum color grades are D, E, F, G, and H.

The highest clarity grade is flawless and, next to that, internally flawless. Stones of such quality are exceedingly rare, however. Even the next-highest clarity grade, VVS-1, is difficult to find on the investment market. The difference between a VVS-1, which stands for very, very slight inclusion of the first degree, and a diamond that is flawless or internally flawless is the presence in the VVS-1 of one to three tiny pinpoint inclusions in the stone. These only affect the grade when visible under ten-power magnification. As the number and size of inclusions increase, under the GIA clarity rating system, the grade drops from VVS-1 to VVS-2 to VS-1 to VS-2. Clarity grades below VS-2, like SI-1 and SI-2 and lower, are not acceptable as optimum investment-grade stones.

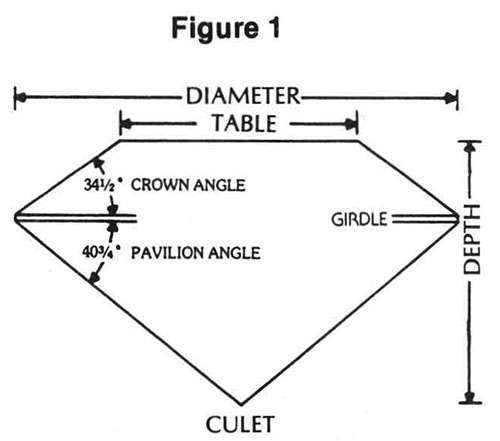

The cut, or "make," of a stone refers to the stone's physical dimensions, computed as ratios and expressed as percentages. The ideal investment stone is the round brilliant cut with 58 facets. Often, in order to save a portion of a rough diamond that excels in color and clarity, a diamond will be cut in a familiar round brilliant shape but not exactly according to the classical blueprint for that cut. To the degree that it varies from the classical exemplar in dimensions and shape, a diamond loses value. The GIA certificate for a diamond shows the stone's depth percentage, crown angles, and table sizes. The depth percentage reflects the relationship between the diameter of the diamond and its depth (Figure 1). Acceptable investment diamonds have a depth percentage between 58 and 63. The ideal crown angle for an investment stone is 34½ degrees. The crown angle will not be mentioned at all on the GIA certificate unless it is 30 degrees or less. The table size is a percentage expressing the relationship between the table, or the flat top of the stone, and the diameter of the stone measured at the girdle. For investment stones, the table percentage should range between 54 and 65 percent, with 60 percent preferred.

Reason

No "pedigree." By this time it should be obvious that the descriptive details of the GIA certificate are absolutely necessary in determining a stone's value. Yet many diamond houses palm off diamonds without GIA certificates! They rationalize that GIA does not evaluate diamonds under one carat—which is not true. People who say that are marketing diamonds with a brand "X" certificate that does not indicate poor crown angles. The California GIA labs have always graded smaller carats, and they always indicate poor crown angles (30 degrees or less), which rates a major reduction in that particular diamond's value.

Buying a diamond without a GIA certificate is like buying an automobile from a juvenile delinquent on a street corner without an automobile title certificate. The GIA certificate shows physical factors that determine value, but it also contains information that identifies a diamond so that the investor can be sure that the stone purchased is the diamond referred to in the certificate. For example, a micrometer is used to measure the dimensions of the stone. Like snowflakes and fingerprints, no two diamonds are exactly alike. Some diamond houses claim they are staffed by GIA graduates using GIA standards. In the same breath they mention the word certificate. But the paper presented upon delivery is not a GIA certificate and will not be accepted as certification by diamond professionals. This is important for two reasons: the diamond is usually worth less than represented because its color, clarity, or cut is not as claimed; and without a GIA certificate the diamond is hardly liquid if the buyer decides to sell.

"I can get it for you wholesale." Many diamond houses claim to be selling at wholesale or at wholesale prices. The term wholesale is a misnomer. Something that is not sold for resale cannot be sold at wholesale, and investment diamonds are not sold to be sold again at retail. Rather than selling diamonds at a set price—the price to the broker—and charging a brokerage fee, diamond dealers have been selling diamonds at a sale price that includes their profit. Most diamond dealers have mark-ups of over 35 percent; some even go over 100 percent. A few have mark-ups considerably below 35 percent.

Leverage. Using a "leverage contract" can be called trading diamonds on margin. A prospective diamond investor with $10,000 who is interested in buying a diamond for $10,000 is told that twice the amount's "value" can be "tied up" at current prices by using the $10,000 as a down payment and paying off the balance in usually six monthly installments with a little interest. There is one diamond house that even allows you five years to pay off your purchase. No diamond is delivered until final payment is made. Before delivery, however, the diamond house representative tells the investor that diamonds have risen in price and prospects look good for further increases—virtually always a truthful statement. The representative then suggests a "roll over" of the position originally costing $20,000 and now worth, say, $25,000 to "tie up" diamonds worth $40,000 to $50,000. Still, no diamonds have been delivered.

The nagging question is: Are those diamonds you are purchasing really there? Or is the whole thing a gigantic Ponzi scheme with no diamonds or very few diamonds to be delivered, with the investor merely moving from one diamond investment position to another on paper only? And some of these leverage contracts are not even on paper. The big danger with this musical chairs game is that the music might stop and you might not get a chair. There are many variations of leverage contracts in diamonds, and some are better than others. For example, a contract to buy specific diamonds in installments with delivery upon full payment maximizes safety in a leverage diamond contract.

The liquidity problem. Investment diamonds are today where gold and silver were in the years 1968-70. Then, liquidity of precious metals was not optimum, but those who invested in metals of proven intrinsic value before precious metal investments became popular realized gains as liquidity increased. Such investors hoped to hedge against inflation. That they did, and more. Eventually competition forced a stabilization of gold and silver prices by narrowing the gap between the bid price and the ask price. Price quotes from markets became common, so that today an investor can make one phone call and find out the current price of gold and silver.

As with precious metals, the liquidity problem in diamonds is being solved by increased competition and volume caused by the popularity of diamonds as an investment. One wire house, or large investment broker, dealing in securities as well as other investments, Shearson Hayden Stone, has formed a company, Polygon, to deal in diamonds. This is a significant step in bringing liquidity to the diamond market because a buyer can be sure of selling a diamond in a known price range on the same day it is purchased if he or she wants to. E.F. Hutton is another wire house considering the brokerage of investment diamonds. In France, the Rothschild Bank and the IndoSuez Bank are already offering diamond investment programs.

Diamond brokers, as expected, are optimistic about the liquidity of investment diamonds.

Gerry Hauser of La Jolla Diamonds, a company that buys as well as sells investment diamonds, told this writer: "We handle the liquidity problem by affiliating with a member of the New York Diamond Dealers Club, one of 14 international diamond bourses. This maximizes the current liquidity. Nevertheless, we recommend holding a stone for at least 18 months and preferably longer before selling. This time period not only assures maximum liquidity; it exceeds the required holding period for capital gain treatment of any realized gain instead of tax treatment as ordinary income. Those who invest in diamonds do so as a hedge against inflation and are not interested in short-term gain or in speculating in the diamond market. Some investors 'liquidate' by trading their diamonds for real estate or other forms of property. For instance, you might have a stone appraised at $60,000 which cannot be sold immediately for more than $50,000 but which someone might exchange for real estate worth $60,000."

On the whole, the prospects for better liquidity in investment diamonds are bright. Liquidity is likely to be a factor in the rise of the price of diamonds the way it was in the rise of the price of gold in the early 1970s. So an investor who buys diamonds now before the coming increase in liquidity should realize the same sharp gains realized by early gold investors.

Buy back. The government objects to diamond sellers' promising to buy back a diamond at any price. No doubt this is supposed to "protect" people, but the government's reasoning here is as specious as the justification for government intervention at all. Nevertheless, buy back plans are tricky, and you can get less than you bargained for.

A typical plan involves a promise by the seller to buy the diamond back discounted 15 percent from the seller's list price, plus the seller charges an additional two percent handling fee to cover the seller in market fluctuation. One diamond house tacks on a buy-back commission to the sales price of the diamond when the diamond is sold to the investor. Such liquidity insurance is costly because the investor may never sell the diamond or may sell the diamond through another house, but he still pays the buy-back commission.

The low ball. Mystery still surrounds diamond pricing. An investment diamond dealer may offer, as an example, a one-carat round-cut diamond of fairly good proportions with a clarity grade of VVS-2 and a color grade of F for a bargain $7,000. Unlike security purchases, a diamond deal can never be consummated until the stone actually changes hands. When the dealer goes to the operations manager of the diamond house he finds out, to his chagrin and the investor's, that that particular diamond just happened to be sold as the representative was discussing this transaction with the investor. But, fortunately for the investor, there is another good deal in the inventory that just came in: a VVS-1, G color, 1.05-carat round diamond of better proportions. The price is $10,000. The first, bargain deal was in fact commercially impossible. The second is not good but is realistic and is profitable for the diamond house. If the prospect does not want to invest more than $7,000, a different-quality stone that is not such a good deal can easily be found in the inventory. This stone—one-carat, VS-2, F color—is the one the dealer had in mind all along.

As with buying a new car, the low ball is an effective sales technique because of the many variables that go into pricing. In automobile pricing the variables are automatic transmission, power windows, bigger engine, tape deck. In diamond pricing, the variables are carat, size, clarity, color, table and depth percentages, etc. The many variables in diamond pricing and the interplay between them make it difficult for the investor to spot the gap between the low ball and the commercially feasible price.

The rip off. One reason why investors buy diamonds is for their hard-money features—intrinsic value held anonymously by the investor. This trait of diamond investing is frustrated by the so-called leverage contract. It also is frustrated when stones are turned over to another for any reason, such as certification by a diamond laboratory or appraisal. A wise buyer always asks for a purchase order or confirmation describing the deposit and setting a value, even if this "value" is less than the actual value of the stones. Otherwise, the buyer has no proof of ownership.

Another rule: never show a diamond dealer or anyone else two stones at the same time, but wait until the first stone is examined and taken off the table before the next stone is displayed. Examination of two stones at the same time facilitates a switch of a stone of lesser value or even a fake diamond. Of the fake diamonds, the most realistic is cubic zirconium, a man-grown crystal with a weight about 1.5 times that of diamonds but worth only about $60 per carat.

Again, the GIA certificate and a check with a micrometer to make sure the diamond offered is the one referred to in the certificate protects the buyer from a switch of a phony stone for a diamond. A good way to ascertain the authenticity of a diamond is to instruct the seller to mail the diamond through GIA, which then certifies not only the grading of the diamond but also the authenticity.

DIAMONDS FOR PROFITS

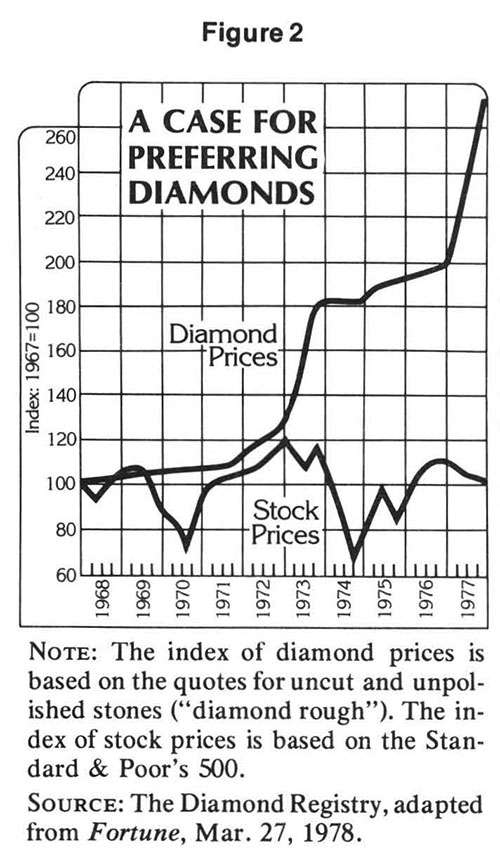

Figure 2 shows the performance of diamonds compared to stocks. Note the smooth, steady, upward rise in investment diamond values. Prices are set by DeBeer's marketing arm, the Central Selling Organization, headquartered in London. This sales entity markets 85 percent of the world's diamonds. When demand is low, it withholds supply, and in the first half of 1978, for example, DeBeers placed four surcharges on rough diamonds in fulfillment of its stated objective of supporting market stability.

Reason

This writer does not advise diamonds as a medium for tax fraud. What the harried American investor does with the anonymity and the portability of his or her diamonds is none of this writer's business. As with foreign tax havens, merely keeping wealth cloaked with anonymity is not a crime even under the Internal Revenue Code. The taxpayer becomes a "criminal" by government standards when the existence of property is denied on a financial statement or when income in the form of gain is not reported on tax returns. The fact that such "crimes" are hard to detect when anonymous wealth is kept in the form of diamonds does not make tax evasion any less a "crime." It merely reduces the government's ability to detect the "crime" and to prosecute.

Perhaps the greatest potential loss in government revenue resulting from the anonymity and portability of diamonds comes in the area of death taxes. An elderly or dying taxpayer with property that appreciated, for instance, from $100,000 to $1,100,000 may well be tempted to liquidate his recorded property holdings and purchase $1 million worth of anonymous and portable investment diamonds to distribute to the objects of his bounty. This lifetime giving is subject to the federal gift tax, which is the same as the federal estate tax and which can be over 70 percent. Even if the cynical entrepreneur once submitted a truthful financial statement to the government or to a bank (same difference), the missing million cannot be traced to the recipients of this "criminal" largesse without their help. Perhaps Daddy Warbucks lost the proceeds from the sale of the estate in Las Vegas or Atlantic City. If the diamond transaction is discovered, which is unlikely in this scenario, that young gold-digger whom Daddy had ensconced in a condominium had cajoled the old fool into giving her those diamonds, thereby defeating the valid probate claims of bereaved heirs, etc.

About the only recourse available to the IRS is setting aside a transfer they can only imagine, assessing imaginary transferee liability, or using their "indirect method" of determining income by computing net worth based on visible purchases, bank deposits, or expenditures. If members of Daddy's family keep their mouths shut and do not flaunt their windfall, the IRS forage is frustrated.

Daddy did not just become a "tax criminal" in the twilight of his life. He probably rode the rising price of diamonds, selling for a gain, failing to report it, and replenishing his diamond investment portfolio with lower-priced stones in the unlikely event he needed diamonds to show the tax collector that he still had the original stones in the same number and even the same total carat weight. He probably gave the diamond broker a fictitious name.

Such opportunities, illegal though they may be, do not present themselves with foreign tax havens. Diamonds are, indeed, a tax haven at home.

John Joseph Matonis practices "antigovernment law" in San Diego, Calif., and Washington, D.C. He has won two cases against Food and Drug Administration regulations. Since 1973 he has been defending against the IRS's assault on property and freedoms.

Board

Chairman, Jon Matonis, and Managing Director, Liza Aizupiete, both

co-founders of Globitex spoke at the Cryptoeconomy Conference in London

on January 26, 2018. The following text summary was transcribed from audio:

Jon: I want to start off by saying something about the three functions of money. If

anyone takes an Economics 101 class, the first thing you learn in

monetary economics are the three functions of money. You have a store of

value, a medium of exchange and unit of account. Those three functions

are required for what economists refer to as a functionary monetary

unit.

Now

the confusion around it though is that they don’t all start at the same

time. They don’t start with unit of account and go backwards, there is a

specific sequence to these functions of money for it to evolve into a

successful currency.

An

example with Bitcoin was the first transaction, the famous pizza

transaction which would be about a $79 to $80 million pizza right now.

Actually it was two pepperoni pizzas. But that’s the current value of

the Bitcoin that was exchanged for that transaction. It was a

transaction from Florida to London.

The

reason people take something in exchange as a medium of exchange is

because they believe that it has value for them after they accept it.

They may not want to hold it but they may want to exchange it obviously

for something else. It starts with store of value which is the first

state that you have to have for anything to evolve as money. Then it

moves to a medium of exchange. It can’t happen the other way around

because it doesn’t make any sense for people to accept it if they don’t

think that it will have at least enough value for them to hold it and

get rid of it.

Then

the last function is a unit of account this is the final stage of

money. This is when you see goods and services priced in the dominant

fiat. So you go shopping in the store in the UK or Europe and on the

shelves it will say pounds or euros, this is the unit of account.

Bitcoin is not there, no cryptocurrency is there yet. This stage takes a

long time to get to unit of account because the government with legal

tender has such an advantage in this area through the requirement of

paying taxes and so forth that it’s very difficult for a newcomer to

break into the unit of account phase. When it happens though it will be a

massive disruption.

People

are already starting to price their services in Bitcoin, but because it

is so volatile they usually price it in another currency and then

through that currency they receive Bitcoin. So that’s not really a unit

of account. But one of the things that will be required to achieve a

unit of account is to have raw basic commodities priced and traded in

the digital currency which is Bitcoin. This is one of the things that

Globitex strives to achieve in this phase of its rollout, the trading

pairs of Bitcoin and raw commodities. So gold, silver, industrial

metals, crude oil, agricultural commodities, for example. This will

start to set, at least at a wholesale level, set the framework and the

basis for using cryptocurrencies as a unit of account which will

complete the three functions of money.

I’m

not just making this stuff up, you can go to a Bank of England report

and they have the same diagram where you have the nested functions of

money.

People

always ask me what do I fear most about the Bitcoin economy? What keeps

me up at night? If I’m such a believer I must have something that I

fear. What do I think will kill Bitcoin? Something like regulation, do I

fear regulations? OK none of those are things that I fear about

Bitcoin. What I fear the most is what is actually happening in the gold

market right now. And I fear that we will get to a point where the

exchanges themselves are successful but we will have

government-sponsored, state-sponsored trading where they will be able to

suppress the price artificially because they have an unlimited supply

of fiat.

There

are a lot of people that believe the gold market today is

suppressed — prices don’t reflect what would really be happening if it

were a true check on central banking. This is possible because unlimited

fiat can be used to do naked short selling on exchanges. The paper

market for Bitcoin in the futures exchange can be manipulated through

price suppression by making naked short selling. Naked short selling is

where you sell the commodity without actually owning it. Exchanges allow

this and it’s legal, you just have to have a certain amount of margin,

the exchanges have to manage contract limits and they have to warehouse a

certain amount for physical delivery.

Now

what is the remedy for this though? This is what keeps me up at night.

Eventually, I think the Bitcoin market will be manipulated in the same

way that gold and silver markets are. The remedy to this is to have

enough global exchanges, enough exchanges worldwide in different

jurisdictions, and even some that may be jurisdictionless. It doesn’t

matter if they are centralized or decentralized, what we need as a

defense is to have enough of these so that a single country or a few

leading governments can’t control a certain exchange. It’s very easy

with gold because most of the gold, paper gold, is traded in New York so

it’s very easy to suppress the price through one exchange that has the

majority of the supply. With Bitcoin we don’t have the mature exchange

market yet, but to the extent that we can get this globally we will be

able to apply the remedy before the attack that I fear.

This

happens to be one the feature of Globitex as well, I mean obviously

we’re going to be one of those exchanges in that ecosystem, but we’re

not going to be the only ones. We’re going to need several thousand

exchanges in different jurisdictions. Leading to the other point that I

wanted to make is, what is the next stage in all of this? So we have a

functioning currency which is a store of value and a medium of exchange.

We have exchanges that are spread out globally in various

jurisdictions, what is the next part of the evolution? Well, this is

what I hear from a lot of my client companies, is that they have no way

to hedge the balance sheet risk that they’re currently holding.

There

are a lot of companies that have Bitcoin and other cryptocurrencies on

their balance sheets, the only way to hedge that is to sell it, sell it

in the physical market, and remove the risk. They can sell it in the

futures market now for the last month, but that’s the cash settlement

market, not a physical settlement market. So it’s a little bit like the

tail wagging the dog when you have cash settled market without the

actual underlying thing being delivered. This allows them to at least

reduce some of that balance sheet risk without having to sell the

commodity. So it’s very helpful but still not 100% effective.

What

I think is going to happen in this space is futures will lead to an

options market where you have call option and put option, you’ll be able

to pay a premium for a call option and a put option. And you’ll be able

to protect the assets on your balance sheet for a known price. This

happens all the time in other multicurrency corporations, they’re using

derivatives to hedge that risk. At Globitex, the futures and options

market is one of the planned phased rollouts, but physically settled. So

they’re physically settled on the futures side.

The

other thing is that when we get to that stage, and we’re already

starting to see it, we start to see an interest rate market develop for

Bitcoin, and Ethereum. The Bitcoin interest rate, does anyone want to

take a guess at what the annual interest rate is for Bitcoin? It’s about

28–35% annually right now. It’s been as high as 350%.

The

reason we know what the interest rate is because the short sellers have

to borrow a Bitcoin in order to sell it. There’s an active two-way

interest rate market for Bitcoin. You only borrow it for a day or a

week, and the rates fluctuate between 28–35%. It’s very volatile so

sometimes it goes over 35%. Now I have named that index Bibor, so it’s

like Libor but it’s Libor for Bitcoin. So it’s a Bitcoin interbroker

offered rate. That is going to be a product one day, and that product

and that forwards curve, that interest-rate and the maturities schedules

that come out of that are going to be used in capital finance for the

crypto-economy. That’s why I love the name of this conference here

because we’re building the early capital markets for a new currency. It

can’t function any other way, it needs to have an interest rate.

So

Globitex will also be market maker in that interest rate curve. So just

like we have interest-rate futures now for the dollar, for the Euro,

you’re looking at overnight, one week, 30 days those will be the

maturities also for cryptocurrencies that are traded on crypto

exchanges. And to give you more color around that and more details

around that I want to introduce my co-founder at Globitex. She will do a

close-up look at what Globitex is planning. We’ve just completed a

successful private pre sale, so we are currently closed for any sales.

So this won’t be a sales pitch, I want to welcome my co-founder Liza.

Liza:

Thank you, my name is Liza Aizupiete. First I’m going to tell you a

little more about what Globitex is, second, I’m going to present a case

for and against a very popular notion of centralized versus

decentralized exchanges. Then I’m going to talk about why we are here,

and what actually got us started. And finally I’ll conclude with our

actual token sale, which is basically looking into the future of what

Globitex is planning to do.

So

first of all Globitex is actually an institutional grade crypto-fiat

exchange. Globitex was recently awarded an EU EMI license which is an

unprecedented license in this space for cryptocurrency businesses,

because it gives us the ability to actually act as our own bank for Euro

payments across the SEPA payment system. Which means for Euro payments

we actually don’t need to integrate with an intermediary bank, we will

be able to issue our own IBAN accounts.

Next,

we have the features of what actually makes Globitex special. Obviously

we’re not the first-comers, we are quite the latecomers to the

industry. But what actually makes us special is that we have a

completely functional API which actually, to date it would be fair to

say that none of exchanges have up to the level that we have developed.

The FIX API gives you a direct market access. Obviously, we also support

Rest API and web sockets. We are running a superior matching engine

with over 1 million transactions per second capacity. If you are a

market maker or a high-frequency trader, you will absolutely enjoy

working on our exchange.

Now

added to that, we are proudly touting our reporting tool. Something so

basic that every broker and every exchange should have. And we have

taken our time to actually develop it to a detail where you can pull

something called the net asset value. Something not everybody

understands or everybody needs, but if you’re an institutional broker,

or accountant, you would definitely appreciate the ability to have a net

asset value report on all trading activities. Our professional trading

platform features a well designed GUI interface for day and night

traders, and you can switch between night and day modes. You can also

choose to move around the modules of the trading platform, so it’s very

customizable.

Finally,

obviously there’s a lot of security that has been worked into Globitex

as a central custodian for cryptocurrencies. We have Bitcoin, Bitcoin

cash, soon Ethereum and Litecoin wallets. And as I already mentioned we

are EMI licensed, so it’s an amazing development, completely

unprecedented in this space and we’ll be very proud to deliver on that

and soon upon full integration with SEPA-MMS system.

Now

here’s the case for and against centralized and decentralized

exchanges. I totally agree with a decentralized monetary system because

this is a thing. As for an exchange there is actually a difference. So

here are the differences. For a decentralized exchange you still need to

do a KYC/AML, in fact in Europe following the banking directive you

will actually be forced or compelled to register and actually disclose

your personal details. By disclosing your KYC you are submitting these

details to a centralized service provider. Therefore by definition, even

if the transactions take place off chain, identification is already a

central point. Obviously for a centralized exchange, identification is

disclosed and centralized, it’s a standard adhering to AML laws.

For

volume, for decentralized exchanges you’re absolutely limited by the

on-chain transaction capacity, which is around seven transactions per a

second for Bitcoin. For Ethereum, in theory, maybe 15 to 30 per second

on a good day but that’s it. So on-chain transactions on a decentralized

exchange are very limited. Whereas for centralized exchanges it is

unlimited, and as mentioned, Globitex supports over one million

transactions per a second. Now, of course you are still able to exchange

on a decentralized exchange, in a limited way, whereas on a centralized

you can list so many things.

Globitex

will be listing futures, options, all the various types of securities

which cannot actually function on a decentralized exchange, it just

doesn’t work, due to transaction speed limitations, impairing price

discovery and liquidity. You need one centralized point of reference,

one point where all of this is clearly listed, quickly executed and

settled. And of course, you need several exchanges to do that, but these

must be centralized.

As

for use cases, obviously decentralized exchanges are going to be

exclusively peer-to-peer, whereas for centralized exchanges enable

global trade, hedgings, speculating, various types of investment. All of

that is enabled by centralized exchanges. It is very biased of course

because I am with a centralized exchange, Globitex is a centralized

exchange and it cannot really be a decentralized exchange unless we

solve the transaction speed per second issue. Maybe once we have

streaming prices I think we can revisit that. And if the regulator is

also on board with it perhaps one day it’s going to be all

decentralized.

So

this is just a very quick reminder of why we are all here, having

listened to the presentations of this wonderful conference. I just

thought that we need to take a look back and see why we’re all here.

Obviously it’s because of Bitcoin, Bitcoin came about and basically

changed pretty much everything. So just a couple of points, Bitcoin is a

distributed completely decentralized network of payments. It doesn’t

sleep on Saturdays or Sundays, like SWIFT or SEPA. The most important

however is that in 2015 on October 22nd here in Europe, Bitcoin was

actually defined as a currency. So on that date the European Court of

Justice pronounced that Bitcoin should be exempt of VAT. Which means

that it is effectively a means of payment and currency.

Now

speaking of exchanges, which diversified further our development into

becoming not only a spot cryptocurrency exchange, but actually go after

the next license, which will enable us not only peer-to-peer lending,

enabling interest rate futures, enabling commodity futures and token

indices futures. We are going after a regulatory approval and system

revamp in order to be able to actually become an exchange for securities

trading, that’s huge.

So

for our Globitex GBX ICO, the fact that cryptocurrencies are here to

stay, this is our basic premise. Bitcoin or bitcoin protocol based

crypto-economy scaling can be achieved by providing better market access

and more diversified product offering. The liquidity issue can also be

solved by developing cryptocurrency money markets to find an equilibrium

between supply and demand. Because money, if you think about it, is

also a thing with an inherent demand and supply. And only when and if

there is enough of a possibility for that demand and supply to meet,

only then would we truly see the relative value of that thing which in

our case is cryptocurrency.

We

believe that Globitex can be instrumental in scaling the cryptocurrency

economy by listing standardised derivatives instruments in money

markets and commodities with both cash settlement and physical delivery,

with bitcoin or Bitcoin protocol-based cryptocurrencies as the unit of

account.

Now

we have seen various types of tokens and ours is going to be a utility

token. Here’s the thing, you will be able to settle trades with the

Globitex GBX token. And if you’re an owner of our token you’ll also

participate in loyalty programs, which we envisage as market making

activities. We would incentivize you to actually help us make market or

provide liquidity by making that trade extremely profitable for you.

When we list futures, from gold to crude oil futures and we need market

makers to participate, we will be incentivizing you to use your tokens

to provide market on these new listings. So it’s a utility token not

only for you, but also for us, as an exchange. The token supply is

limited, or calculated at a €10 million market hard cap. The redeemed

tokens will be burned, and taken out of the circulation, therefore the

Globitex GBX token is deflationary, limited in supply and therefore

should be appreciating in value.

Let’s not deploy the nuclear option for every protocol upgrade.

Make no mistake. We are witnessing a high-stakes protocol standards

battle play out in real time. And it is just as important as last

century’s battle for the internet’s TCP standard.

Current capacity constraints on the Bitcoin blockchain have brought us to this impasse.

The

Bitcoin protocol, as the dominant value transfer “network effect”

leader, battles against upstart cryptocurrency protocols like Ethereum

and Monero. But it also battles with itself as divergent forces push for

either on-chain scaling or off-chain scaling, hard fork or soft fork, SegWit transaction format or original transaction format.

The

so-called nuclear option is a prolonged, contested hard fork of the

Bitcoin blockchain because it risks splitting the network into two

competing chains, which is to no one’s benefit. Therefore, it should be

reserved as a planned formality or a last resort for extreme situations

rather than a perpetual form of “live” dispute resolution.

With so

much individual and institutional wealth essentially stored on the

Bitcoin blockchain, it can be extremely disconcerting when others try to

“fork” around with your money. Chronic forking is not synonymous with

wealth management and prudent capital accumulation, which require

stability and predictability. Importantly, smart contracts and

non-monetary applications will also rely upon relative stability since

the same native digital token also facilitates the proof-of-work

security model.

This article will examine how open-source

governance was designed to work within the Bitcoin protocol and how

users, miners and developers are locked in a symbiotic dance when it

comes to potential forks to the immutable consensus. Solutions will be

proposed and analyzed that maintain the decentralized nature of the

resulting code and the blockchain consensus, while still permitting

sensible protocol upgrades. Governance is not only about the particular

method of change-control management, but also about how the very method

itself is subject to change.

Open-Source Protocols and Bitcoin

Generally

referred to as FOSS, or free and open-source software, this source code

is openly shared so that people are encouraged to use the software and

to voluntarily improve its design, resulting in decreasing software

costs; increasing security and stability, and flexibility over hardware

choice; and better privacy protection.

Open-source governance

models, such as Linux and BitTorrent, are not new and they existed prior

to the emergence of Bitcoin in early 2009; however, they have never

before been so tightly intertwined with money itself. Indeed, as the

largest distributed computing project in the world with self-adjusting

computational power, Bitcoin may be the first crude instance of A.I. on

the internet.

As

a blockchain community grows, it becomes increasingly more difficult

for stakeholders to reach a consensus on changing network rules. This is

by design, and reinforces the original principles of the blockchain’s

creators. To change the rules is to split the network, creating a new

blockchain and a new community. Blockchain networks resist political

governance because they are governed by everyone who [participates] in

them, and by no one in particular.

Murck continues:

Bitcoin’s

ability to resist such populist campaigns demonstrates the success of

the blockchain’s governance structure and shows that the ‘governance

crisis’ is a false narrative.

Of course it’s a

false narrative, and Murck is correct on this point. Bitcoin’s lack of

political governance is Bitcoin’s governance model, and forking is a

natural intended component of that. “Governance” may be the wrong word

for it because we are actually talking about minimizing potential

disruption.

Where Bitcoin differs from other open-source protocols

is that two levels of forking exist. One level forks the open-source

code (code fork), and another level forks the blockchain consensus

(chain fork). Since there can only be one consensus per native digital

token, chain splits are the natural result of this. The only way to

avoid potential chain splits in the future is to restrict the

change-control process to a single implementation, which is not very

safe nor realistic.

Core development teams are a potentially dangerous source of centralization.

When it comes to Bitcoin Core,

the publicly shared code repository hosts the current reference

implementation, and a small group of code committers (or maintainers)

regulate any merges to the code. Even though other projects may be more

open to criticism and newcomers, this general structure reminds me of a

presiding council of elders.

Making hazy claims of a peer-review

process or saying that committers are just passive maintainers merely

creates the facade of decentralized code. The real peer-review process

takes place on multiple community and technical forums, some of which

are not even frequented by the developers and Bitcoin Core committers.

The BIP (Bitcoin

Improvement Proposal) process is sufficient and it’s working for those

who choose to collaborate on Bitcoin Core. Similar to the RFC (Request

for Comments) process at

the IETF, BIP debates about a proposed implementation can provide

technical documentation useful to developers. However, it is not working

for many involved in Bitcoin protocol development due to the advantages

of incumbency and the false appeal to authority with core developers.

If Bitcoin Core no longer maintains the leading reference implementation

for the Bitcoin protocol, it will be 100 percent due to this

intransigence.

Sensitive to the criticisms of glorifying Bitcoin Core, Adam Back of Blockstream recently proposed an option to freeze the base-layer protocol,

but at the moment that will only move all of the politics and

game-playing to what exactly the base-layer freeze should look like. It

is a nice idea for separating the protocol standard from a single

reference implementation and for transitioning the Bitcoin protocol to

an IETF-like structure, although it’s extremely premature for now.

Therefore, by default, that leaves us with several alternative Bitcoin implementations in an environment of continual forking.

Even Satoshi Nakamoto was critical of multiple consensus implementations in 2010:

I

don’t believe a second, compatible implementation of Bitcoin will ever

be a good idea. So much of the design depends on all nodes getting

exactly identical results in lockstep that a second implementation would

be a menace to the network.

“All code that impacts consensus is part of consensus,” Voskuil told Bitcoin Magazine.

“But when part of this code stops the network or does something not

nice, it’s called a bug needing a fix, but that fix is a change to

consensus. Since bugs are consensus, fixes are forks. As such, a single

implementation gives far too much power to its developers. Shutting down

the network while some star chamber works out a new consensus is

downright authoritarian.”

Multiple alternative implementations of the Bitcoin protocol strengthen the network and help to prevent code centralization.

Politics of Blockchain Forking (or How UASF BIP 148 Will Fail)

Contentious

hard forks and soft forks all come down to hashing power. You can

phrase it differently and you can make believe that two-day zero-balance

nodes have a fundamental say in the outcome, but you cannot alter that

basic reality.

A BIP 148 fork

will undoubtedly need mining hash power to succeed or even to result in a

minority chain. However, if Segregated Witness (SegWit) had sufficient

miner support in the first place, the BIP 148 UASF itself would be

unnecessary. So, in that respect, it will now proceed like a game of

chicken waiting to see if miners support the fork attempt.

Mirroring

aspects of mob rule, if the UASF approach works as a way to bring

miners around to adopting SegWit, then the emboldened mob will deploy

the tactic for numerous other protocol upgrades in the future. Consensus

rules should not be easy to change and they should not be able to

change through simple majority rule on nodes, economic or not.

Eventually, these attempts will run headfirst into the wall of Nakamoto consensus.

As far as the network is concerned, it’s like turning off the power to your node.

UASF BIP148 Nodes (1st August 2017)

There

is no room for majority rule in Bitcoin. Those who endorse the UASF

approach and cleverly insert UASF tags in their social media handles are

endorsing majority rule in Bitcoin. They are providing a stage for any

random user group to push their warped agenda via tyranny of the nodes.

The prolific Jimmy Song says that having real skin in the game is what matters:

Bitcoin

doesn’t care if you post arguments on Reddit. Bitcoin doesn’t care if

you put something clever in your Twitter name. Bitcoin doesn’t care if

you educate people, write articles, or make clever Twitter insults.

Bitcoin doesn’t care about your wishes, your feelings or your arguments.

Let’s

keep “majority rule” antics out of Bitcoin. There is no protocol

condition that activates “if we are all united” and that is a good

thing.

With enough hashing power, the mob-induced UASF BIP 148

will lead to a temporary chain split. However, the probability of a

Bitcoin minority chain surviving for very long is extremely low due to

the lengthy difficulty re-targeting period of 2,016 blocks. Unlike the

Ethereum/Ethereum Classic fork, that is a long time for miners to invest

in a chain of uncertainty.

Responding to a Reddit post for newbies who are scared of losing money around the 1st of August due to UASF, ArmchairCryptologist explains:

Your

advice is sound, but realistically, the most likely scenario is that

the UASF either wins or dies. If it gets less than ~12% of the hashrate,

it will not be able to activate Segwit in time, and it will almost

certainly die. If it gets less than ~20% I also wouldn’t be surprised to

see active interference with orphaning to prevent transactions from

being processed.

If on the other

hand it gets more than ~40% of the hashrate, the chance for a reorg on

the other chain is large enough that most miners will likely jump ship,

and it will almost certainly win. At over ~20% block orphaning attacks

won’t be effective, as it would split the majority chain hashrate and

risk tipping the scale. Which means that the only situation where you

will realistically have two working chains for an extended period is if

you get between ~20% and ~40% of the hashrate for the UASF.

The

collectivist UASF BIP 148 strategy will ultimately fail and that’s a

good thing. It is driven primarily by those with very little at stake

expecting the miners to stake everything by supporting a minority chain.

Pretty soon, you run out of other people’s money. This commenter on Reddit understands:

The

entire premise was that it was very cheap to switch, but very expensive

to stay. That’s when I realized the folly of it all; [it’s] only cheap

because they’re not staking anything. But someone has to stake

something.

And that’s what is going to cause it to fail. That and the lack of replay protection. People like this guy flip it around and genuinely believe the mining problem will

be solved by massively increased value. If they do somehow put enough

pressure on exchanges that list UASF, despite the lack of replay

protection, and if we take his logic a step further, UASFers are going

to be pushing everyone to “buy, buy, buy” UASF and “sell, sell, sell”

Legacy Coin. But without replay protection, they’re going to be

obliterated by a few smart people who realize there are huge gains to be

had.

Alphonse Pace has an excellent paper describing

chain splits and their resolution. He walks us through compatible,

incompatible and semi-compatible hard forks, arguing that users do have

power if they truly reject a soft-fork rule change:

…

users do have power — by invoking an incompatible hard fork. In this

case, users will force the chain to split by introducing a new ruleset

(which may include a proof-of-work change, but does not require one).

This ensures users always have an escape from a miner-imposed ruleset

that they reject. This way, if the economy and users truly reject a soft

fork rule change, they always have the power to break away and reclaim

the rules they wish. It may be inconvenient, but the same is true by any

attack by the miners on users.

The Future of Coordinating Protocol Upgrades

What group determines the big decisions in Bitcoin’s direction? Ilogy doubts that it is the developers:

Theymos

almost completely foresaw what is happening today. Why? Because Theymos

has a deep understanding of Bitcoin and he was able to connect the dots

and recognize that the logic of the system leads inevitably to this

conclusion. Once we add to the equation the fact that restricting

on-chain scaling was always going to be perceived by the ‘generators’ as

something that ‘reduces profit,’ it should be clear that the logic of

the system was intrinsically going to bring us to the point we find

ourselves today.

Years later these two juggernauts

of Bitcoin would find themselves on opposite ends of the debate. But

what is interesting, what they both recognized, was that ultimately big

decisions in Bitcoin’s direction would be determined by the powerful

actors in the space, not by the average user and, more importantly, not

by the developers.

The developer role can be thought of as

proposing a variety of software menu choices for the users, merchants

and miners to accept and run. If a software upgrade or patch is deemed

unacceptable, then developers must go back to work and adjust the BIP

menu offering. Otherwise, mutiny becomes the only option for

dissatisfied miners.

In “Who Controls Bitcoin?” Daniel

Krawisz says that the investors wield the most power, and because of

that, miners follow investors. Therefore, the protocol upgrades likely

to get adopted will be the ones that increase Bitcoin’s value as an

investment, such as anonymity improvements being favored over attempts

at making Bitcoin easier to regulate.

In the future, miner

coordination via a Bitcoin DAO (decentralized autonomous organization)

on the blockchain could be the key to smooth and uneventful forking.

Self-governing ratification would allow diverse stakeholders to

coordinate protocol upgrades on-chain, reducing the likelihood of

software propagation battles that perpetually fork the codebase.

Attorney Adam Vaziri of

Diacle supports a system of DAO voting by Bitcoin miners to remove the

uncertainty around protocol upgrades. He readily admits that he has been

inspired by Tezos and Decred.

Prediction

markets have also been proposed as a method to gauge user and miner

preferences through public forecasting, the theory being that these

prediction markets would yield the fairest overall consensus for

protocol upgrades prior to the actual fork.

The question remains:

Is coin-based voting based on allocated hash power superior to the

informal signaling method utilized today? Are prediction markets or

futures markets a viable method to gauge consensus and determine

critical protocol upgrades?

I’m not optimistic. On-chain voting

and “intent” signaling are both non-binding expressions while prediction

and futures markets can be easily gamed. Therefore, while Tezos and

Decred represent admirable efforts in the quest for complete resilient

decentralization, I do not think Bitcoin protocol upgrades of the future

will be managed in this way.

The Bitcoin ecosystem doesn’t need to achieve a social consensus prior

to making changes to the protocol. What has clearly emerged from the

events of this summer is that Bitcoin has demonstrated an even stronger

degree of immutability.

There is no failure of governance and there is no failure of

the market. The non-authoritarian forces at play here are functioning

exactly as they should. Protocol upgrades in a decentralized environment

are an evolutionary process, and that process has matured to the current six stages of Bitcoin protocol upgrading, with some optional variances for BIP 91:

(a) BIP menu choices competing for mindshare, strategic appropriateness and technical rigor;

(b) Informal intent signaling based on miners inserting text into the coinbase for each block mined;

(c) Block

signaling period where miners formally signal a designated “bit”

trigger for BIP lock-in, based on “x” percent over a “y” number of

blocks period;

(d) Block activation period after BIP lock-in,

which sets a secondary period of “x” percent over a “y” number of blocks

for activation;

(e) Primary difficulty adjustment period (2,016 blocks) where “x” percent of miners must signal for the upgrade to lock in;

(f) Secondary difficulty adjustment period (2,016 blocks) required for the protocol upgrade to activate on the network.

Conclusion